Brexit and the ensuing Brexit deal essentially ties the UK auto industry into using either UK or European BEV/battery components rather than depending on imported systems.

Currently, the Rules of Origin (RoO) threshold, before tariffs are applied, is 55% (UK/EU) content. There is an exception for EVs which temporarily enjoy a lower RoO requirement (40%) until 2027 after which time it returns to the normal rate (55%). The battery is key due to its high proportion of total vehicle input cost and its impact on the RoO threshold. The EU tariff for failing to meet this threshold is 10%. Transportation costs associated with imports between regions add to this cost.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

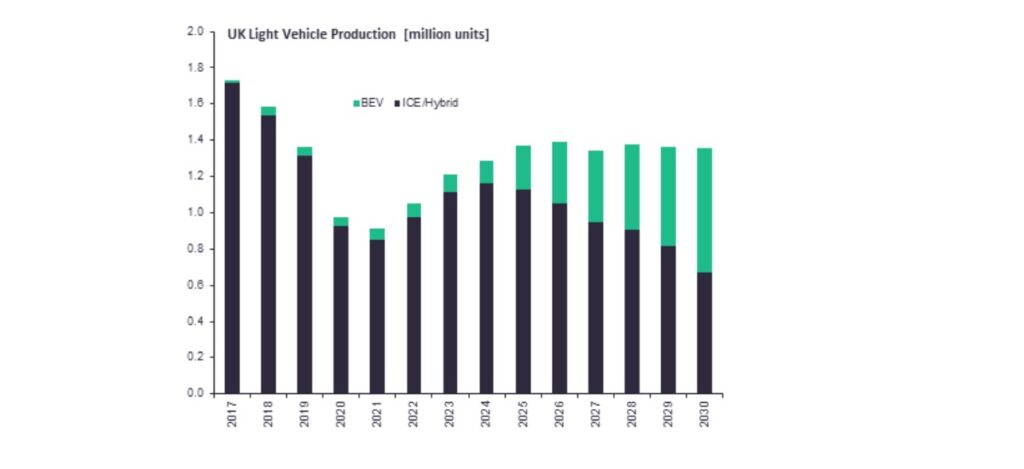

As the shift towards electrification gathers pace, European production sourcing decisions for new BEV capacity is beginning to be formulated with the UK potentially at a disadvantage given the RoO thresholds from 2027.

There are three directions that the UK could take:

- Import battery cells and systems from Europe (as Mini does today)

- Localise UK BEV production using domestic battery suppliers (such as AESC, for example)

- UK does not participate in mainstream BEV manufacturing – leading to the longer-term wind-down of domestic volume auto manufacturing

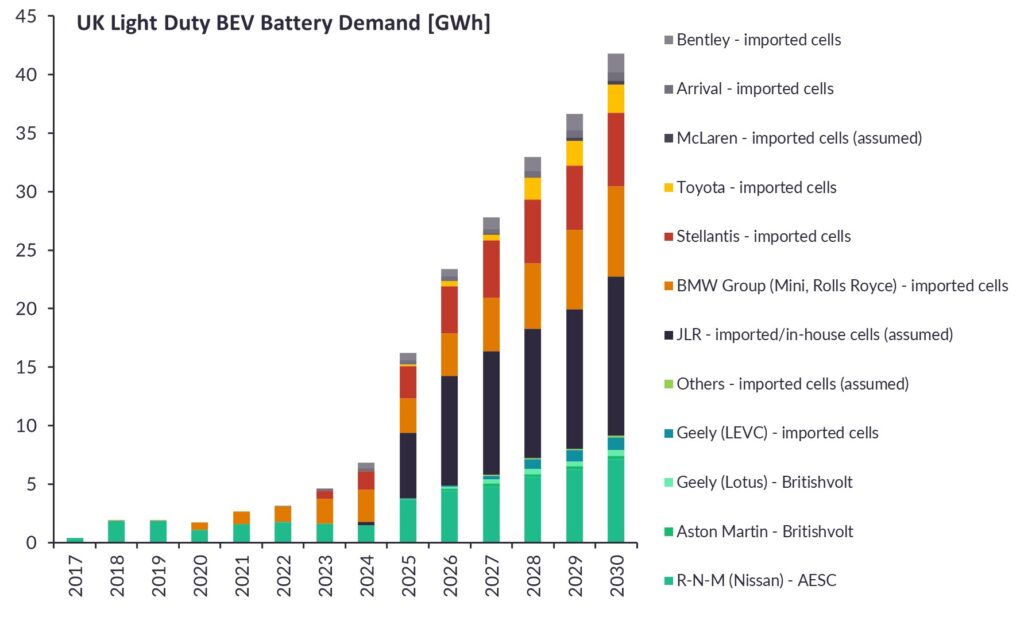

The emerging supply chain picture shows that the majority of demand for battery cells will be satisfied by imports from mainland Europe.

What are the prospects for transitioning to domestic supply?

Most of the domestic supply will be from AESC (for Nissan). So far, Britishvolt has found automotive customers in bespoke cell solutions – and this was always our expectation – but this niche segment does not require a gigawatt scale.

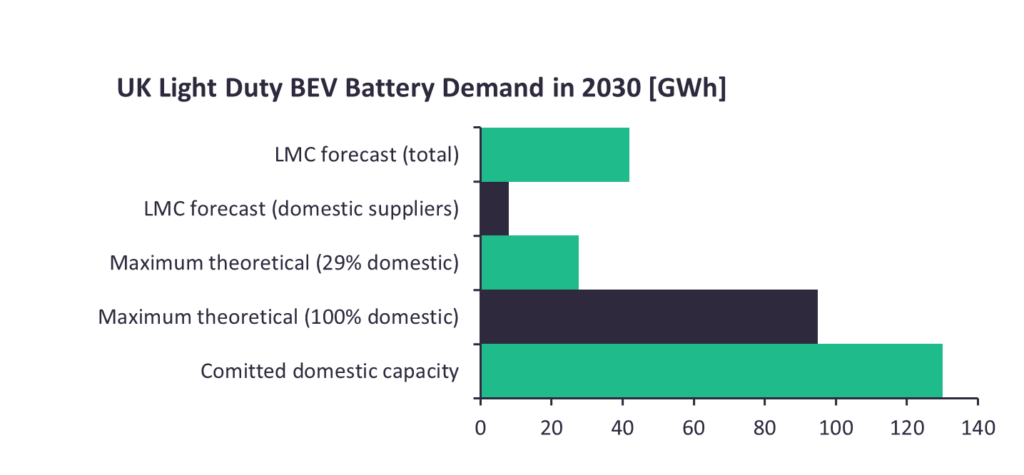

EV batteries are often incorrectly thought of as fungible commodities. An automaker cannot simply take a Britishvolt cell and place it in a vehicle engineered for CATL batteries, without labouring through the multi-year cell qualification process and vehicle development cycle. Therefore, it is unlikely that the UK will move to anywhere near 100% domestic sourcing for batteries in this decade.

What about demand from other applications?

There is certainly room for demand from stationary energy storage, two-wheeler EVs, heavy duty, maritime, aerospace, and other applications, but they will be dwarfed by the light vehicle BEV sector in the meantime, and so do not require a colossal cell production infrastructure within this decade.

In the very long term, demand from stationary energy storage would have to grow to an order of magnitude similar to EV sector if the UK is to meet its net-zero targets.

What about exporting to mainland Europe?

Ever since the UK put up trade barriers with its largest trading partner, exports have been lagging behind all other developed nations during the COVID-19 recovery. It is difficult to imagine automaker customers in mainland Europe choosing UK startups, especially those without a unique selling point or advantage over more established and localised suppliers with whom they have joint ventures. To entice those customers, UK battery suppliers would have to offer a significant competitive advantage, be it in cost, technical edge, or production capability.

There is cause for optimism in the long run:

The UK has a long-standing research base in next-generation battery technologies, along with the government-backed institutions to industrialise them. Britishvolt and other home-grown companies therefore have bright futures as the UK’s cell manufacturing spearheads.

In summary: although not an ideal situation, the UK auto industry can survive without a vast domestic battery manufacturing base. It is lagging mainland Europe in establishing itself as a major cell production hub in the region, but it still has opportunities in serving other areas of the battery supply chain and in leapfrogging contemporary lithium-ion technologies.

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center

Sam Adham is senior powertrain research analyst for LMC Automotive