Battery Electric Vehicle (BEV) technology continues to evolve at an increasingly rapid rate, impacting material costs and consumer affordability. Here Grant Thornton and Cox Automotive highlight the critical component changes disrupting the BEV industry.

Inflated battery costs are impacting the purchase of BEVs – a key takeaway from the seventh issue of its quarterly AutoFocus automotive insight update. Rising raw material costs are bumping up retail prices, impacting and dissuading consumers from purchasing the sustainable vehicle alternative – approximately 60% of a BEV’s price is attributable to its battery cost.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

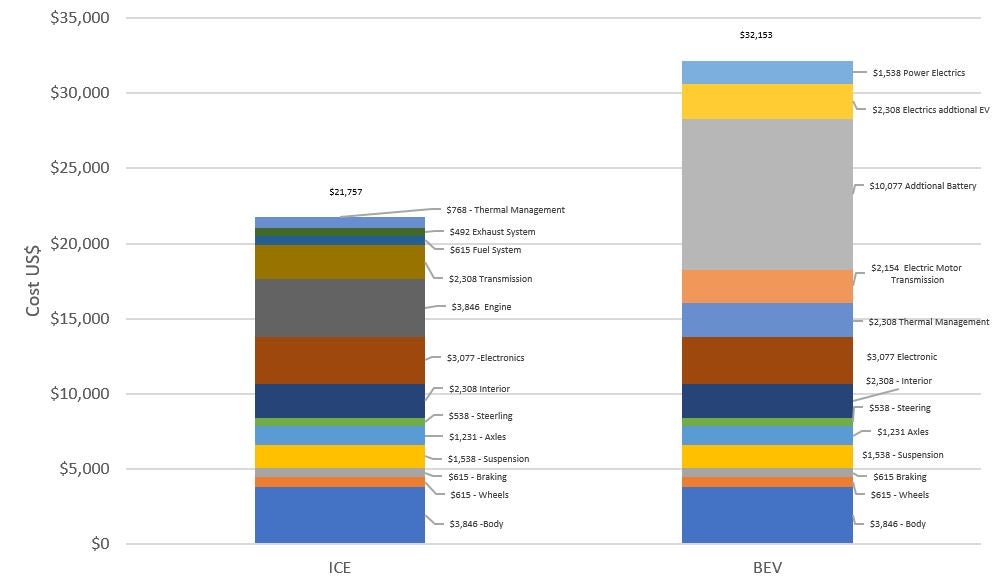

The below chart illustrates the vast disparity between traditional ICE and BEV vehicles, with manufacturers forking out over $10,000 more for a BEV, an upshot of a hefty battery price tag.

Cost of Manufacturing – Petrol Vs BEV

Source Citifirst.com

Consumers and OEMs sharing the load

Soaring battery prices have been underpinned by unprecedented rising raw material costs as demand for lithium, nickel, and cobalt surges, with increases passed on to consumers in recent times.

Philip Nothard, Insight & Strategy Director at Cox Automotive, explains more: “Due to ‘pass-through’ contracts, battery manufacturers do not incur the cost of raw material price hikes; these are attributed to OEMs. Not wishing to see margins drop significantly, vehicle OEMs have been forced to pass on the additional cost to consumers. In addition, lithium, the key component in all lithium-ion batteries, is experiencing elevated demand levels due to BEVs and other battery-operated machinery.”

Cobalt has experienced a slower price increase compared to lithium due to the latter being the most used of all the above raw materials in BEVs. As a result, manufacturers are moving away from using cobalt in batteries where possible and manufacturing different batteries with less or no cobalt. Such a move has changed battery chemistry, which gives both the battery and BEVs distinctive characteristics – charging speed, energy density, and range.

Changes to battery chemistry

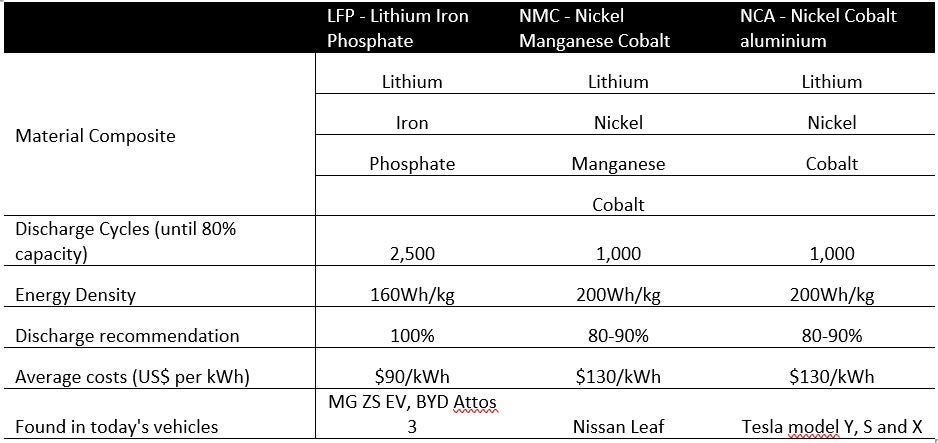

Owen Edwards, Head of Downstream Automotive at Grant Thornton UK LLP, explains, “There are three key battery chemistry technologies for BEVs: NMC, NCA and LFP. Battery chemistry has traditionally focused on NMC and NCA; looking ahead, however, demand for LFP is expected to increase. The LFP battery is not as powerful as NMC and NCA but comes at a lower cost and contains no cobalt. These are just some reasons why Tesla uses this technology in its batteries for the new Tesla 3 series.”

In addition, battery technology is improving as battery size increases. At present, the cylindrical battery 21700 (diameter 21mm 70mm length) is the primary battery type used for Tesla vehicles; however, the move to 46800 batteries, which is significantly larger than the 21700, has reduced the cost of Tesla batteries by US$2,000 to $3,000 per vehicle, due to the reduced number of welds between each cylindrical battery. Nevertheless, the increase in battery type and size is not as straightforward as expected. At present, Tesla is struggling for consistent quality in 46800 batteries; therefore, it is more expensive to manufacture these batteries than the 21700.

Owens adds, “Although continued raw material prices are expected, underpinned by expected demand from BEVs and other forms of transport, battery storage, etc. – it is not clear whether there will be sufficient supply of raw materials to satisfy demand.”

Alternative raw materials and technology

To reduce exposure to expensive raw materials, Tesla has diversified its battery chemistry from NCA to NCM to LFP batteries, now found in the latest Tesla Model 3 manufactured in China.

Nothard adds: “OEMs are encouraged to adopt a similar strategy: reduce costs by selecting different raw materials and battery technologies and, simultaneously, generate the optimum power density while maintaining battery safety. Ultimately the pay-off between cost, power density and battery safety is key; with the reduction in battery costs due to improved technology, vehicle OEMs are moving towards the cost of manufacturing a BEV at parity with ICE vehicles.”

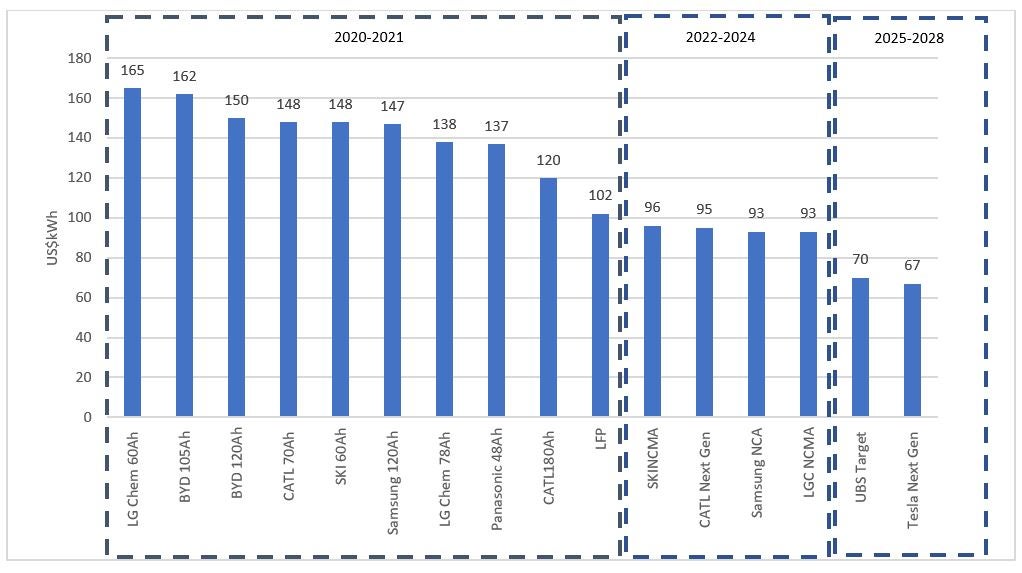

At this future parity point, the total cost of ownership of a BEV will be lower than owning an ICE vehicle, making the BEV an attractive purchase for consumers. It is estimated that the industry battery cost parity to ICE vehicles will be reached between 2025 and 2028.

The Battery Cost Curve

Source UBS

Advances in battery materials

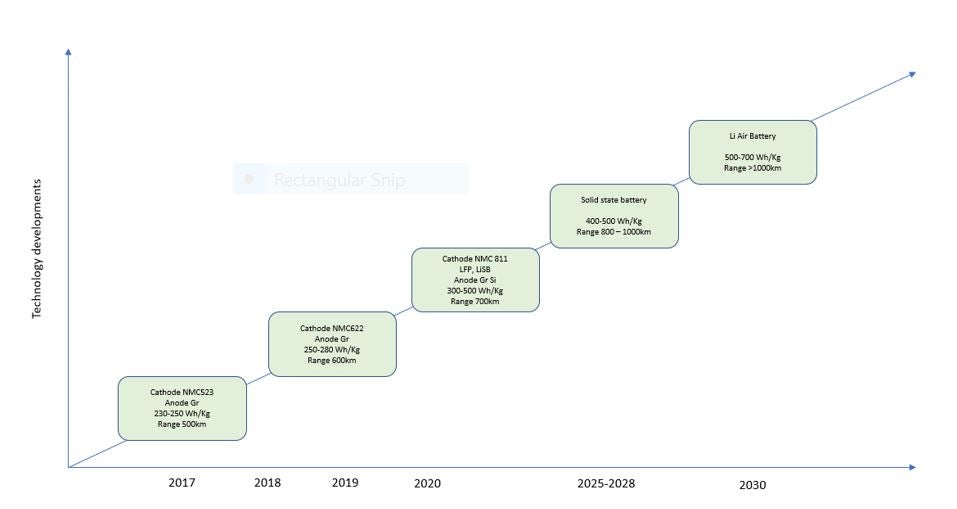

Step changes in battery technology are expected as new battery developments are generated. At present, different battery chemistries are increasing power, range, and charging capability as well as reducing battery costs.

The appeal of investing in cheaper and more abundant raw material batteries, such as lithium-sulphur battery technology (LiSB), continues to grow; however, it’s worth noting that this battery chemistry is likely to be used in battery storage, where there is the requirement for high energy, slow discharge, and low cost. This battery’s chief benefit is its prominent sulphur level, which is abundant and inexpensive to extract. These batteries are expected to be ready for commercial use after 2030.

Solid-state battery technology incorporates an electrolyte made of solid material instead of the current liquid electrolyte batteries. Such a battery offers several advantages, including a higher level of energy density, lower risk of fire, and significantly lower use of cobalt, along with the ability to increase driving range from 600km to 1,000k, depending on the chemistry. Research suggests solid-state batteries will be available by 2026 – 2028.

Finally, Lithium-air battery technology pairs lithium and air with an anticipated battery density of 500-700 Wh/kg, calculated to generate vehicle ranges of more than 1,000km on a single charge. The battery, which is in very early testing and planning phases, is expected to offer a high energy output, enabling vehicles to exceed 1,000km on one charge.

Current and future battery technological developments

Source British Volt and Grant Thornton Analysis

The battery technology of tomorrow

Battery technology is constantly evolving.

Such short-term advancement could lead to increased volatility in vehicle residual values, especially for leased or financed cars with long-term contracts. In addition, with the prospect of a significant technological shift imminent, finance and leasing companies should consider the impact it could have on their vehicle residual values, with the potential risk that some vehicles may become ‘black cars,’ i.e., vehicles which might have an insufficient range/charging capabilities, resulting in extremely limited market appeal and low residual values.

Nothard expands on this: “At present, without knowing when these step changes in battery technology will occur, it is difficult to determine what cars may be ‘black.’ However, a good knowledge of battery technology and future battery development should equip retailers with the tools to minimise exposure to such vehicles.”

Motor finance demand high despite rising cost of borrowing